Should you change investments ahead of the election? Maybe.

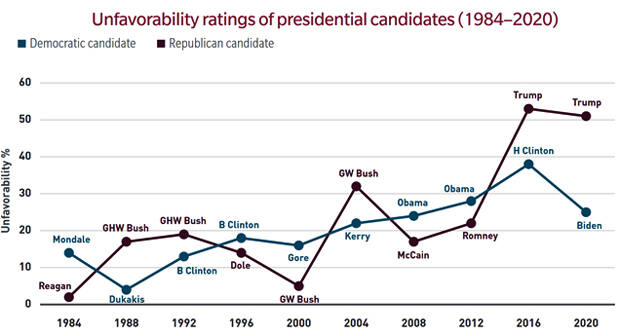

Worried about what might happen to financial markets and your investments if we have the first contested election in 20 years, or if your candidate doesn’t win? You aren’t alone. Unfavorability ratings of presidential candidates has been on the rise the last 36 years and with the megaphone that social media has given the most vocal and polarizing of each political leaning this is a trend that is unlikely to reverse anytime soon. With all of the negative news and information (some real and some not) out there it’s understandable why individual investors would have some concern.

As we discussed last month, individual investors have historically dramatically underperformed the stock market and have underperformed institutional investors even more. Remember, for every winner in the stock market there is an equal and opposite loser. If an individual sells a stock when things are plummeting (like we mentioned a whopping 1/3 of investors 65+ with accounts at Fidelity did in our June article) to an institution and that stock then goes up in price (like most have since then) the individual loses out on an equal amount of gains as what the institution receives. As we mentioned last month, the vast majority (70%) of this underperformance can be contributed to just 10 periods when market volatility had picked up and individual investors acted out of emotion and panic sold. With fear running high during what the media has dubbed ‘the most important election of our lifetime’ (which they seem to do every election cycle) and the world still in the middle of the first global pandemic in a century it makes sense why people would want to ‘wait until things calm down’ if they panic sold earlier this year or might be tempted to sell everything now that there’s been a recovery.

The problem with ‘waiting until things calm down’ is that things are usually calmest right before market drops causing ‘buying high’ followed by panic when things drop and ‘selling low,’ the exact opposite of what you want to do. So what should you do? Stay invested if you are already invested or ‘buy and hope’ (our term for the ‘buy and hold’ investment strategy) that things go up if you’re one of the people that’s been sitting in cash contributing to the record amount in money market? Or should you stay in cash or move to cash?

READ: Who believes in the S&P 500 rally?

My answer: probably neither. We could certainly see large gains or large losses and it is important to be in good position for either. If you have a million dollars and you miss out on a 10% gain by sitting in cash it’s the same as being fully invested and experiencing a 10% loss. Either way, you are missing out on $100,000 the only difference is that in one case you had the $100,000 and then lost it rather than not having it and missing out on it. It’s important to have an investment strategy that can do well in a rising market, but also take advantage of a volatile one. That way you can thrive regardless of whatever happens with the market either because of or in spite of the election and its result.

Don’t mix politics with your portfolio. There were far too many investors that missed out on amazing gains when the last 2 presidents were elected because they thought things were not going to go well because their candidate lost. The first year Obama was in office the S&P 500 returned 26% while the first year under Trump yielded a similar 22% gain. The first year after every recent election has actually been the best performing and the years after ‘where things have calmed down’ have had far fewer gains. Emotions are high right now, especially in this election cycle, but don’t let it drive your investment decisions.

The largest strategy we are utilizing in our client accounts currently is designed to have good gains if markets should rise and has historically outperformed the most when things are rocky. In the last 2 years we’ve certainly seen rockiness with the first 2 selloffs of over 20% in more than a decade, but this particular strategy has outperformed by over 30% all while taking on a ton less risk.

How has this been accomplished? By losing a lot less during declines and taking advantage of them by getting more aggressive as things fall resulting in similar returns when the market is going up. There is the most opportunity for outsized gains when markets are uncertain and volatile, not when they are calm. As Warren Buffett famously said during 2008 ‘be greedy when others are fearful and fearful when others are greedy.’

Unfortunately most retail investments products and managed accounts available to retail investors are of the ‘buy and hold/hope’ variety and only do well when markets do well as they are 100% invested 100% all the time and don’t deviate much between their makeup of US stocks, foreign stocks, bonds, cash, etc. over time even if one of these is performing poorly or expected to continue performing poorly. We think this is unfortunate, but the good news is there are some out there that not only don’t suffer from this inflexibility, but have consistently blown away the competition over time with a lot less risk.

So how do you find strategies like this? Well, the first place to look if you are looking at mutual funds is in the fund’s prospectus or annual report. There you will find what the goals of the fund are and how it goes about investing. You want to look for funds that aren’t trying to beat their peers and/or an index(es) (meaning an international fund trying to outperform other international funds or an international stock index or a moderate risk fund trying to beat other moderate risk funds or a specific index combination), but rather have goals like ‘make up all losses within a 3 year time period while outperforming the stock market over the long term’ or ‘achieve a high investment return with reasonable risk with no limit or minimum on how much is invested in stocks, bonds, or money market.’ Many of these types of investments have really shined the last few years and have done well when markets go up, but have done even better when things are falling. Given that no one knows who the winner of the election might be or how it might impact the markets, it would be wise to look at investments that can prosper regardless of what happens.

If you’re near or in retirement certainly having one with a goal to make up all losses within 3 years can help relieve anxiety too. Why? Because if you know there is a good chance you’ll be in a worst case scenario back to even in 3 years and have at least 3+ years worth of income sitting in investments that are more conservative, you don’t have to worry about short term fluctuations (whether they be from a virus, election, or something else) impacting your ability to have the income you want and need in retirement.

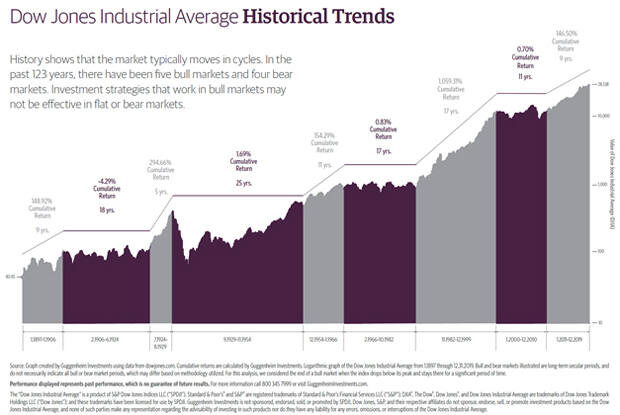

Buying traditional stock strategies or funds that are always 100% invested, particularly those that follow indexes, historically would have resulted in several lengthy time periods that investors would have had to wait a long time to get back to even. Looking at the Dow Jones Industrial average below you can see that over the last 123 years we’ve had an 18 year, 25 year, 17 year, and 11 year time period where there was little to no return. These time periods make up 71 of the 123 years, which is nearly 58%!

Having an investing strategy that not only does well when markets go up, but really prospers when they don’t isn’t just important with an upcoming election. It’s been important for more than a century since the Dow Jones began! If what might happen with the election has you worried about your portfolio most likely the problem isn’t politics; it’s how your portfolio is constructed or managed.

If you don’t have the time or expertise to go through and research every investment out there (there’s over 322,000 that the research team at Morningstar tracks) to find one that’s appropriate for your financial situation/goals that doesn’t just do well when market are going up, considering speaking with a financial professional that does. At The Retirement Team the majority of the assets we manage are invested in these types of strategies not only because it makes a ton of sense given the pandemic and current political and economic landscape, but because during the majority of the history of the stock market they would have led to a more successful retirement. If you’re already working with an advisor and they have you positioned in an antiquated ‘buy and hold/hope’ approach instead of one like this, consider speaking with another. It is impossible to say when or how long the next red area from the Dow Jones chart may be, which is why we believe it’s important to have a more dynamic approach that still does well in good times, but really excels in bad.

Material discussed is meant for general/informational purposes and is not intended to be used as the sole basis for any financial decisions, nor be construed as advice to meet your particular needs. Please consult a financial professional for further information. The Dow Jones Industrial Average cannot be invested in directly. Investing in securities involves risk and profit cannot be guaranteed.

Investment advisory services offered through Next Generation Investing, LLC.

Securities offered through World Equity Group, Inc. member FINRA and SIPC.

Next Generation Investing, LLC, & The Retirement Team are not owned or controlled by World Equity Group.

Insurance and annuities offered through Ryan Shumaker, KS Insurance License #10359614.

Ryan can be contacted at 785-228-0222 or RetireTopeka.com.