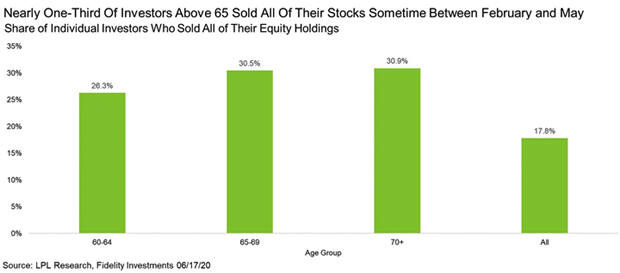

Nearly 1/3 of investors 65+ sold at the stock market bottom

Typically when you fail to plan, you are planning to fail, and that applies to the stock market. It’s best to have a plan before trouble comes, rather than make emotional decisions on the fly during times of duress as this often leads to the exact wrong decision. Incredibly nearly 1/3 of investors 65+ (a group typically in or near retirement) sold 100% of their investments in stocks or stock mutual funds between February and May of last year; a time in which stocks were down significantly.

One year since stocks hit their bottom on March 23rd the S&P 500 is up 68.9%, the Dow Jones Industrial Average is up 75.9%, and the Nasdaq is up a whopping 95.2%! It is clear that many that sold exactly at the wrong time are still sitting on the sidelines too in cash or money market funds given that there is now currently more money in money market funds than there ever has been in history. In fact, there is nearly twice the amount sitting in cash right now than there was just 5 years ago, according to LPL Research.

READ: How to avoid the new tax increase on retirement accounts

Certainly ‘selling low’ and ‘buying high’ is not a good investment strategy, but unfortunately it is one that far too many that are close to or in retirement are following. The bull market that began in March of 2009 and ended in March of last year is the longest one we’ve ever recorded in the United States. It likely left too many feeling far too confident and then at the first sign of trouble when a few years of gains were wiped out very quickly, panic set in and those losses got locked in by many that sold everything.

It is important to always have a plan ahead of time for not only what to buy and when to buy it, but what to sell and when to sell it. It is also important for those near or in retirement to have a strategy and plan in place for what you’re going to do when markets fall and how you’re going to generate reliable income from your investments during such times. Unless you have a really short retirement it is not a question of if, but when and how many times the market will fall during your retirement. Relying on emotions to guide you on the fly rather than having a plan ahead of time will too often lead to poor outcomes.

Typically when someone first comes into our office they are positioned well if markets perpetually go up, but have no plan and will do poorly when they go sideways or down. It is important to create a plan for those two eventualities as again it is not a question of if, but when and how many times they will occur in the future. Knowing what you’re going to do ahead of time can help lead to better piece of mind, less worry, and less bad decision making, especially if the plan you have ahead of time ensures your retirement income stream will be unaffected by falling markets.

If you are serious about getting such a plan created, our firm is serious about helping. Whether or not there is a second selloff later this year after the large run up we’ve seen should not impact a good, solid retirement plan as a good, solid retirement plan should have a strategy to deal with future market selloffs, regardless of what causes them or when they occur.

Material discussed is meant for general/informational purposes and is not intended to be used as the sole basis for any financial decisions, nor be construed as advice to meet your particular needs. Please consult a financial professional for further information.

Investment advisory services offered through Next Generation Investing, LLC.

Securities offered through World Equity Group, Inc. member FINRA and SIPC.

Next Generation Investing, LLC, & The Retirement Team are not owned or controlled by World Equity Group.

Insurance and annuities offered through Ryan Shumaker, KS Insurance License #10359614.

Ryan can be contacted at 785-228-0222 or RetireTopeka.com.